Summary: Rigs – The total US rig count decreased by 5 rigs for the May 5 week, down to 572 from 577. Infrastructure – Canada’s new Trans Mountain Pipeline expansion is online and transporting crude oil from Edmonton to Vancouver. Storage – East Daley expects an injection of 650 Mbbl into commercial and Strategic Petroleum Reserve (SPR) inventories for the week ending May 17. Regulatory and Tariffs– Seaway Crude Pipeline The temporary incentive discount rates were extended through June 30, 2024.(FERC No 2.85.0 IS24- 269, filed May 08, 2024).

Rigs:

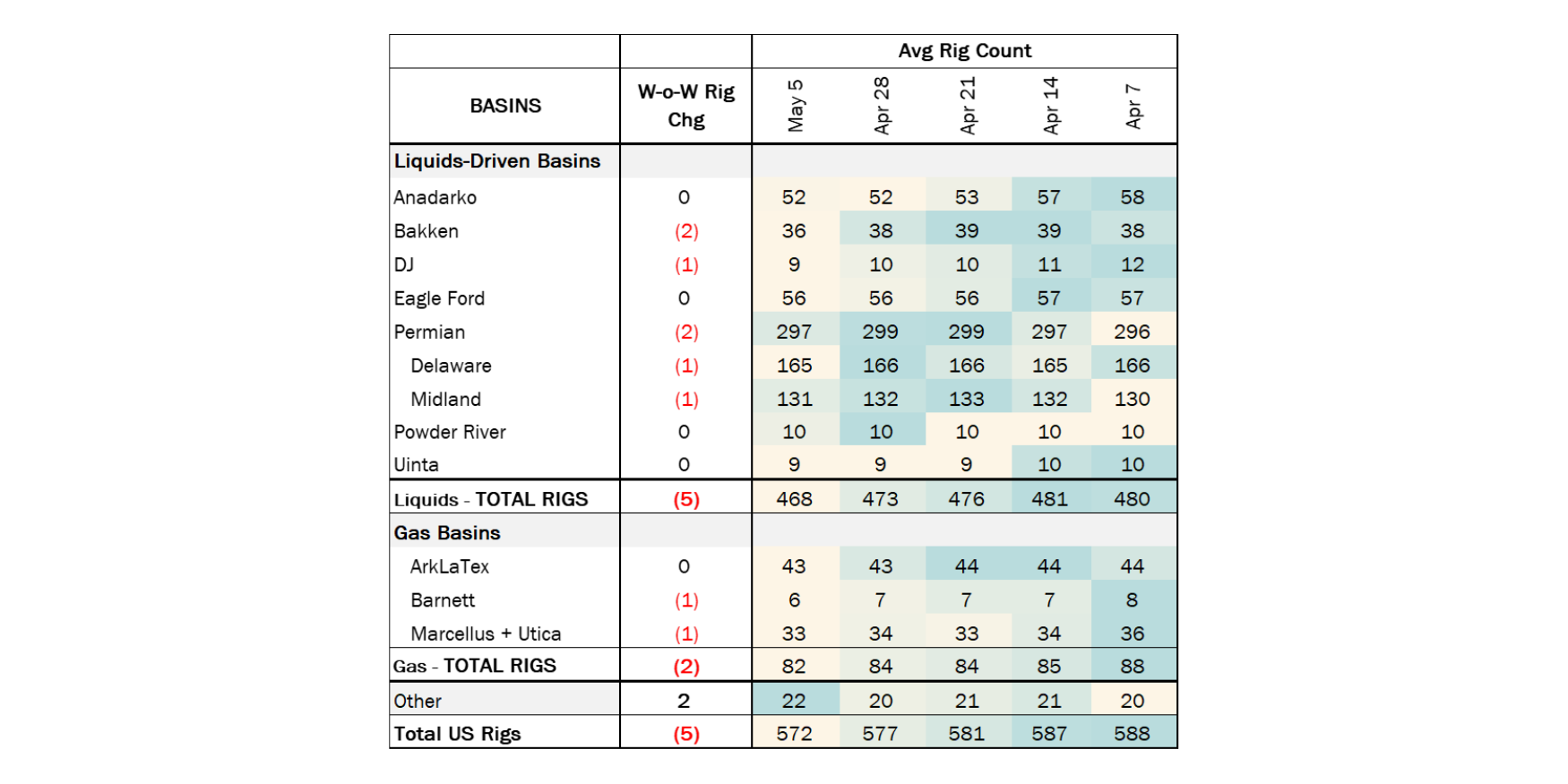

The total US rig count decreased by 5 rigs for the May 5 week, down to 572 from 577. Liquids-driven basins drove the decline, down 5 rigs W-o-W to a total of 468. The Permian and Bakken basins each lost 2 rigs, with the Permian losses split between the Delaware and the Midland. The DJ decreased by 1 rig W-o-W to 9.

In the Permian, Delaware operator Continental Resources removed 1 rig, exiting the week with 5 rigs. Pioneer Resources in the Midland also dropped 1 rig from its program, down to 20 from 21. In the Bakken, Continental Resources and Exxon each removed rigs, bringing the basin total to 36.

Infrastructure:

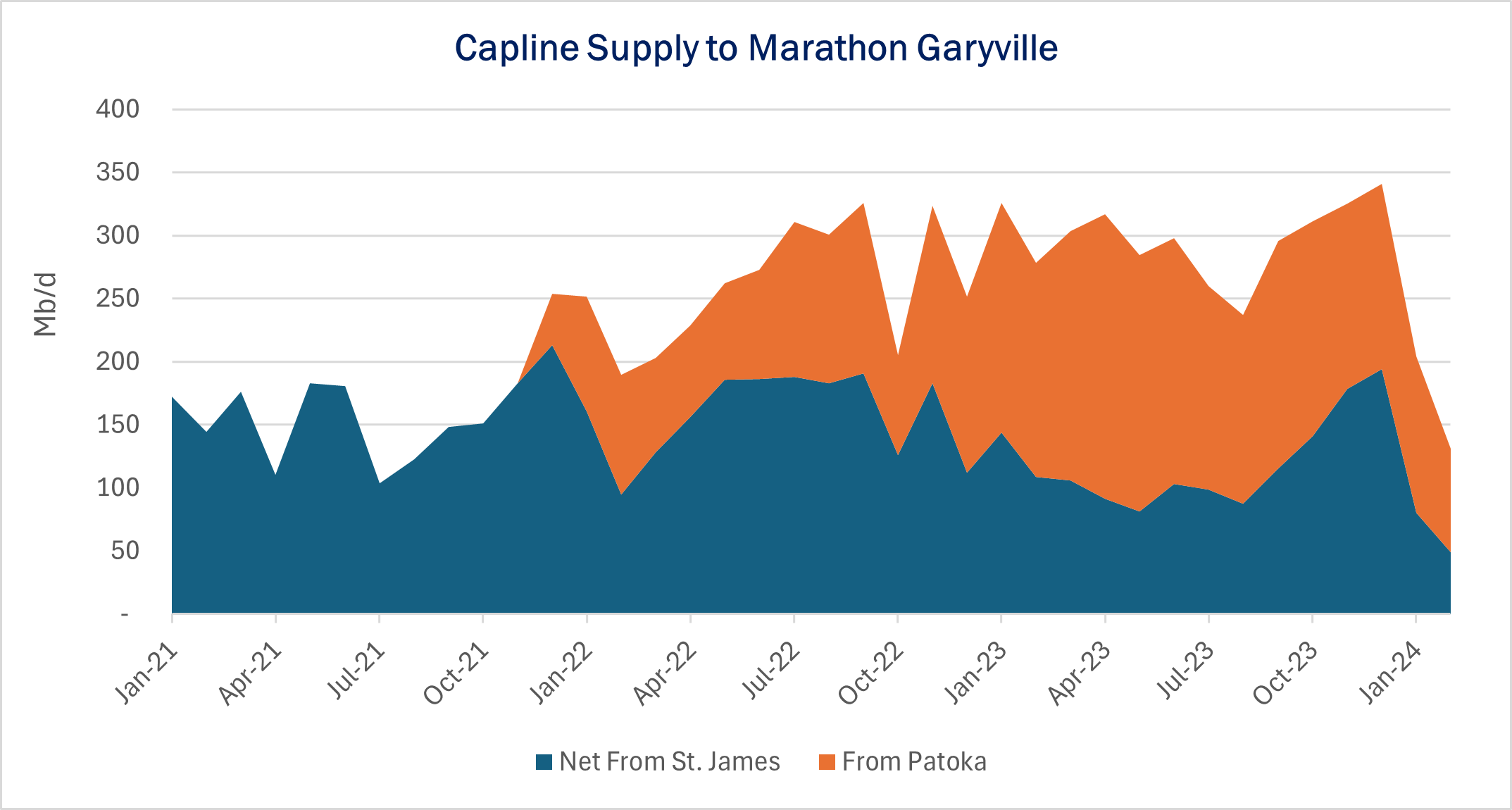

Canada’s new Trans Mountain Pipeline expansion is online and transporting crude oil from Edmonton to Vancouver. East Daley expects the project will initially displace volumes exported to the US, including barrels to Marathon’s (MRO) Garyville refinery in Louisiana.

The Garyville refinery is the sole recipient of crude oil from Capline Pipeline, which moves Canadian heavy sour barrels from Patoka, IL. Since the reversal of Capline Pipeline in 3Q21, crude oil from Patoka does not actually makes its way to the St James market hub in Louisiana. Instead, on the eastern outskirts of St James, the oil is directed to a Marathon pipeline that connects to the Garyville refinery.

Earlier this month, Capline announced an open season offering incentive rates for crude oil of a light sweet quality, further suggesting heavy sour crude from Canada from will be replaced with domestic barrels.

MRO’s Garyville refinery also receives crude oil via the ~520 b/d Marathon Pipeline from St James. East Daley believes Marathon will look to the LOCAP and Ship Shoal pipelines to replace the lost Canadian heavy sour barrels, possibly upsetting the tight supply and demand balance of the St James market.

According to the Crude Hub Model, the St James market totals 1.1 MMb/d, receiving crude oil via pipeline, barge and rail. There are six major refineries in the area with a total demand pull of ~1.8 Mb/d. The refineries augment their supply from the Empire market, Permian Express LOLA Pipeline, and via barged oil from outside of St James.

EDA expects the TMX expansion will have impacts across North America, including in the Gulf Coast where the balance of light sweet crude oil in St James could be altered as local refineries search for alternative supply.

Storage:

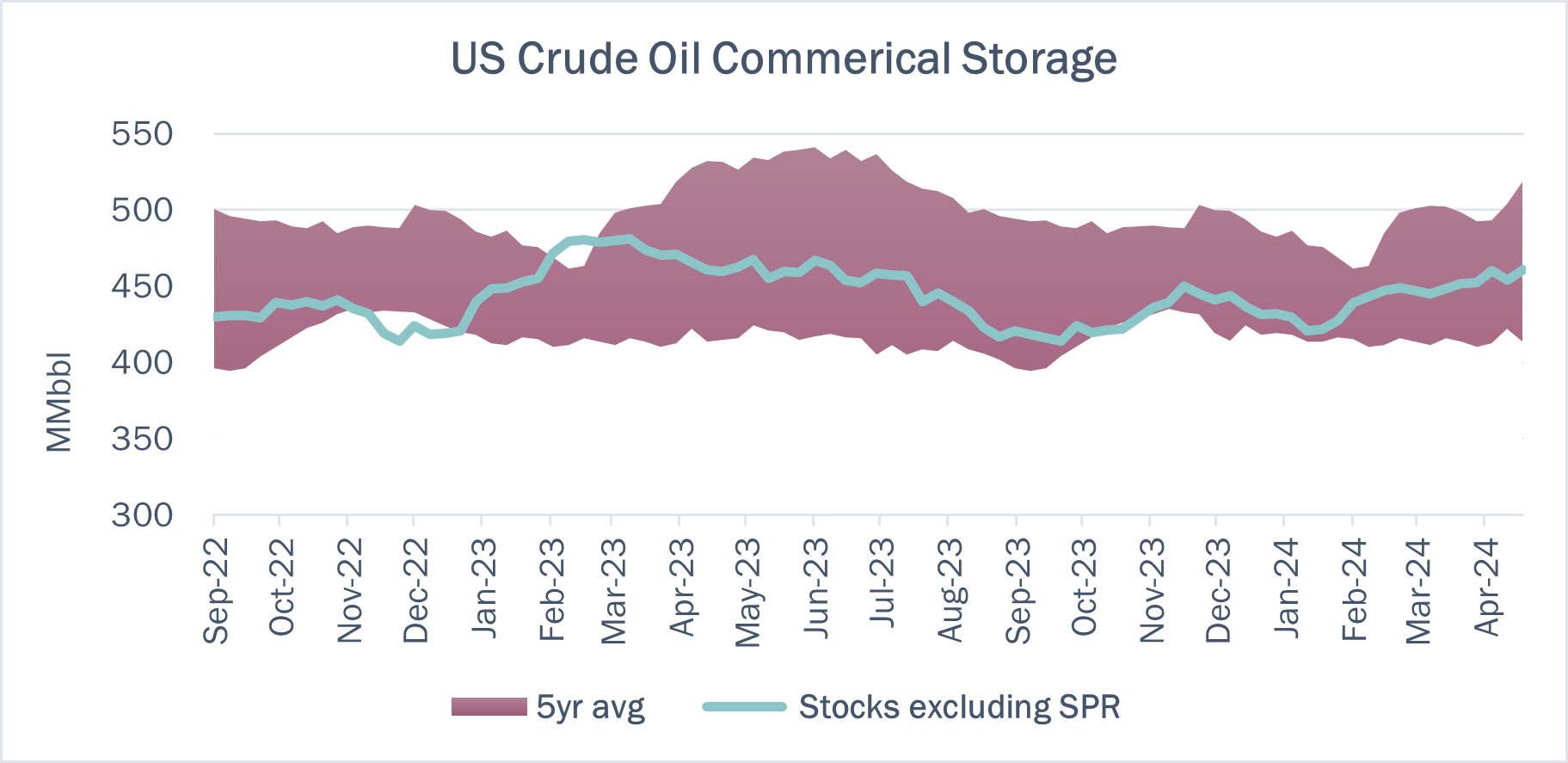

East Daley expects an injection of 650 Mbbl into commercial and Strategic Petroleum Reserve (SPR) inventories for the week ending May 17. We expect total US stocks, including the SPR, will close at 828 MMbbl.

The US natural gas pipeline sample, a proxy for change in oil production, fell ~4.5% W-o-W across all liquids-focused basins. Samples decreased 3.54% in the Rockies and 3.61% in the Gulf of Mexico. The declines were offset by a 2.12% increase in the Permian, 4.23% in the Eagle Ford. The Williston Basin has a very high correlation between gas volumes and crude oil volumes, whereas the Eagle Ford’s correlation is less than 30%. We expect US crude production to remain flat at 13.1 MMb/d.

According to US bill of lading data, US crude imports increased by 156 Mb/d W-o-W to 6.9 MMb/d. More than 60% of the supply originated from Canadian pipelines into the US, with the remainder largely coming from ships carrying crude from Mexico and Argentina.

As of May 10, there was ~409 Mb/d of refining capacity offline, including downtime for planned and unplanned maintenance. EDA expects gross crude inputs into refineries to increase by ~245 Mb/d W-o-W, coming in at 16.5 MMb/d.

Vessel traffic monitored by EDA along the Gulf Coast decreased W-o-W. There were 23 vessels loaded for the week ending May 17 and 27 the prior week. EDA expects US exports to be 4.2 MMb/d.

The SPR awarded contracts for 3.1 MMbbl to be delivered in May 2024. The SPR has 368 MMbbl in storage as of May 10, 2024.

Regulatory and Tariffs: Presented by ![]()

Tariffs:

Seaway Crude Pipeline The temporary incentive discount rates were extended through June 30, 2024.(FERC No 2.85.0 IS24- 269, filed May 08, 2024)

The above information is provided by ARBO’s Oil Pipeline Tariff Monitor. For more information on regulatory proceedings or tariff rates, please contact please contact Corey Brill via email at [email protected] or phone at 202-505-5296. https://www.goarbo.com/