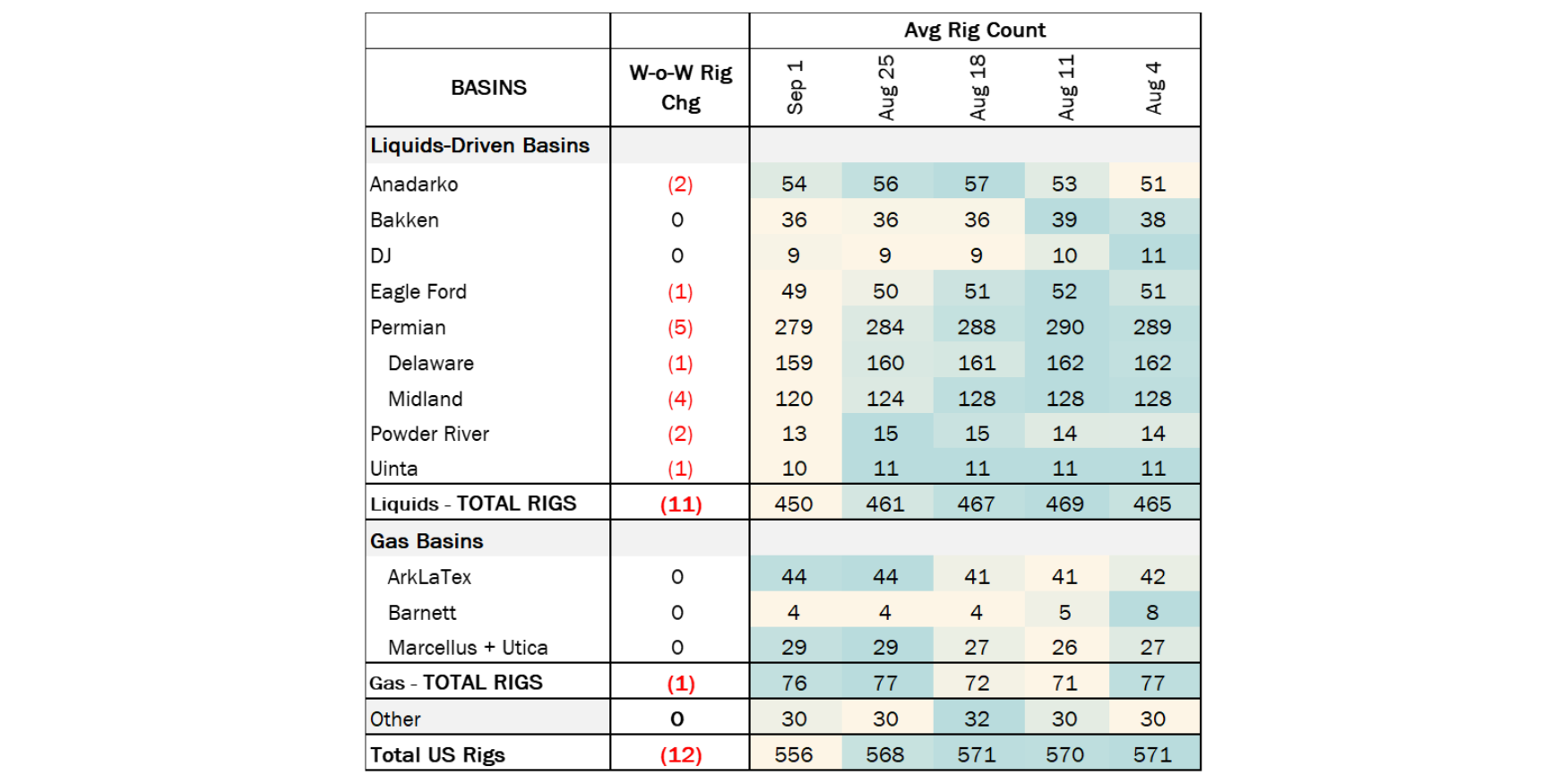

Executive Summary: Rigs: The US rig count decreased by 12 for the September 1 week, down to 556 from 568. Infrastructure: Chevron (CVX) has started production from the deepwater Anchor project in the Gulf of Mexico using new offshore technology for high-pressure reservoirs. Storage: East Daley expects a 417 Mbbl withdrawal in commercial and Strategic Petroleum Reserve (SPR) inventories for the week ending September 13.

Rigs:

The US rig count decreased by 12 for the September 1 week, down to 556 from 568. Liquids-driven basin saw a loss of 11 rigs, decreasing the count from 461 to 450. The Anadarko and Powder River basins each lost 2 rigs whereas the Eagle Ford and Uinta basins each dropped by 1 rig. The Permian Basin saw a loss of 5 rigs while the Bakken region and DJ Basin rig counts remained flat.

In the Anadarko Basin, operators 89 Energy III and Calyx Energy III each dropped 1 rig. In the Eagle Ford, Crescent Energy dropped 1 rig, In the Delaware Basin, operator Devon Energy removed 1 rig. In the Midland Basin, Endeavor Energy saw a decrease of 2 rigs whereas APA Corp. and Texland Petroleum each dropped 1 rig. In the Powder River Basin, True Companies and Hilcorp each decreased rig counts by 1. In the Uinta Basin, Uinta Wax Operating laid down 1 rig.

Infrastructure:

Chevron (CVX) has started production from the deepwater Anchor project in the Gulf of Mexico using new offshore technology for high-pressure reservoirs. Crude oil from Anchor is set to lift volumes for several Gulf Coast pipelines, according to the Crude Hub Model.

The Anchor project includes a semi-submersible floating production unit in water depths of 5,000 feet, located ~140 miles offshore southeast Louisiana. Operator CVX (62.9%) and TotalEnergy (37.1%) started the first platform in August using new technology to produce from deeper, high-pressure offshore fields. Anchor is rated to handle flows at pressures of up to 20,000 psi and reach targets up to 34,000 feet under the surface, CVX said.

Anchor has a design capacity to produce up to 75 Mb/d of crude oil and 28 MMcf/d of natural gas. The partners plan to drill seven subsea wells in the Green Canyon area. The Anchor field has up to 440 MMboe of recoverable reserves, CVX said.

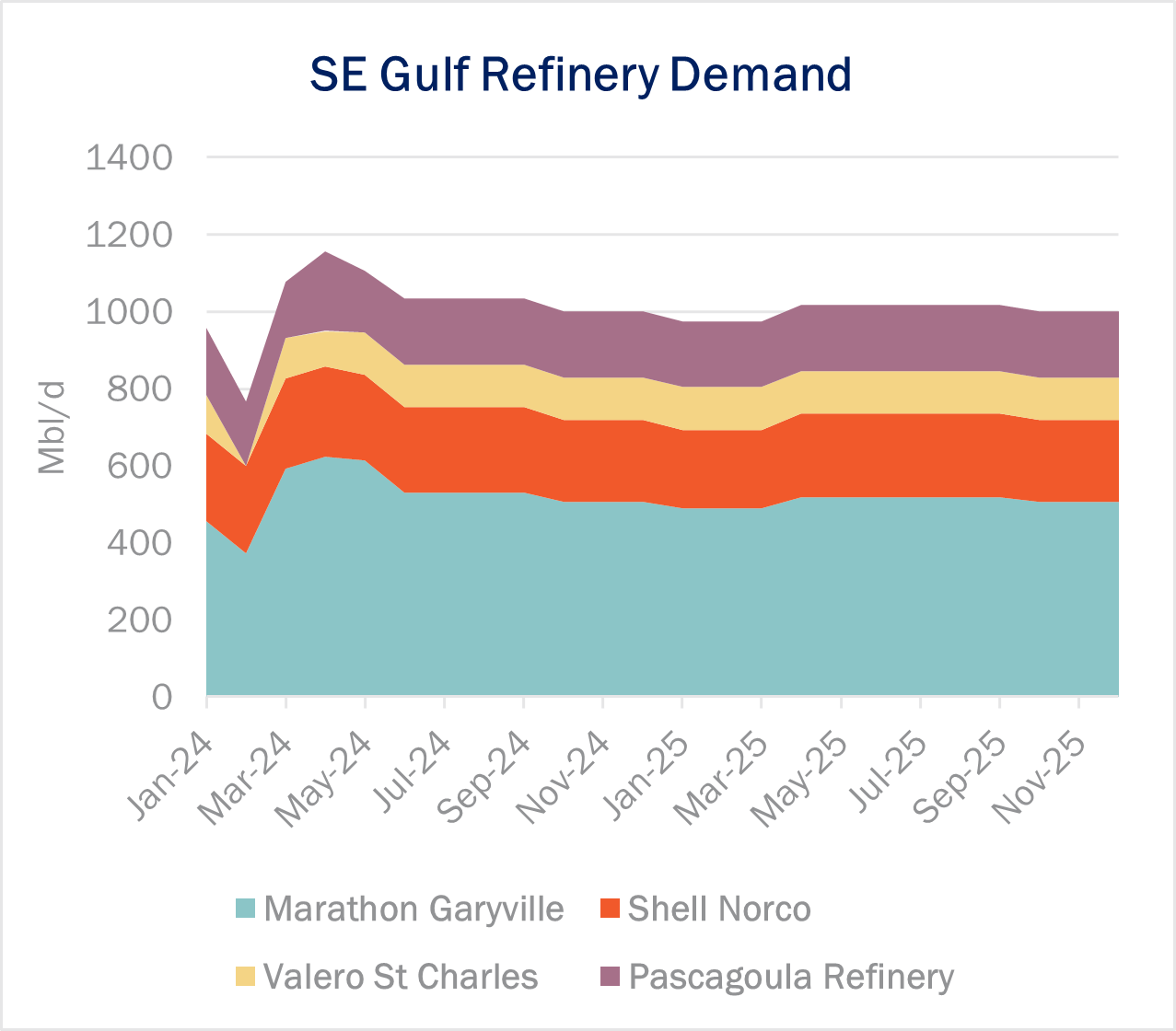

Crude oil from Anchor can grow volumes for several on- and offshore systems in the Crude Hub Model. Much of the oil produced from Anchor will move on Amberjack Pipeline (500 Mb/d capacity), owned by CVX and Shell. Oil on Amberjack travels to Mars Pipeline (600 Mb/d), which can then deliver to the LOOP system (800 Mb/d) and on to the St. James, LA refinery hub. Mars can also deliver to a Chevron pipeline that connects to Empire, LA. Many of those barrels then travel to the Pascagoula refinery in Mississippi on the Cal-KY pipeline.

Based on the Crude Hub Model and SONRIS data, we expect Amberjack Pipeline utilization to remain flat at ~75% for the rest of 2024. Mars Pipeline utilization is also forecast to hold at around 55% for the remainder of 2024. LOOP import utilization is low at around 7% through 2024. Finally, utilization for the Chevron pipeline to Empire holds at ~85% through YE24. So there is plenty of room to move new production to Gulf Coast markets.

Considering that much of the oil from Anchor will end up on LOOP, refineries in St. James and the Pascagoula refinery stand to benefit from more options to pick up barrels. However, we don’t expect the new crude production to increase exports on LOOP (see our August 28 Crude Oil Edge on LOOP for more information).

Storage:

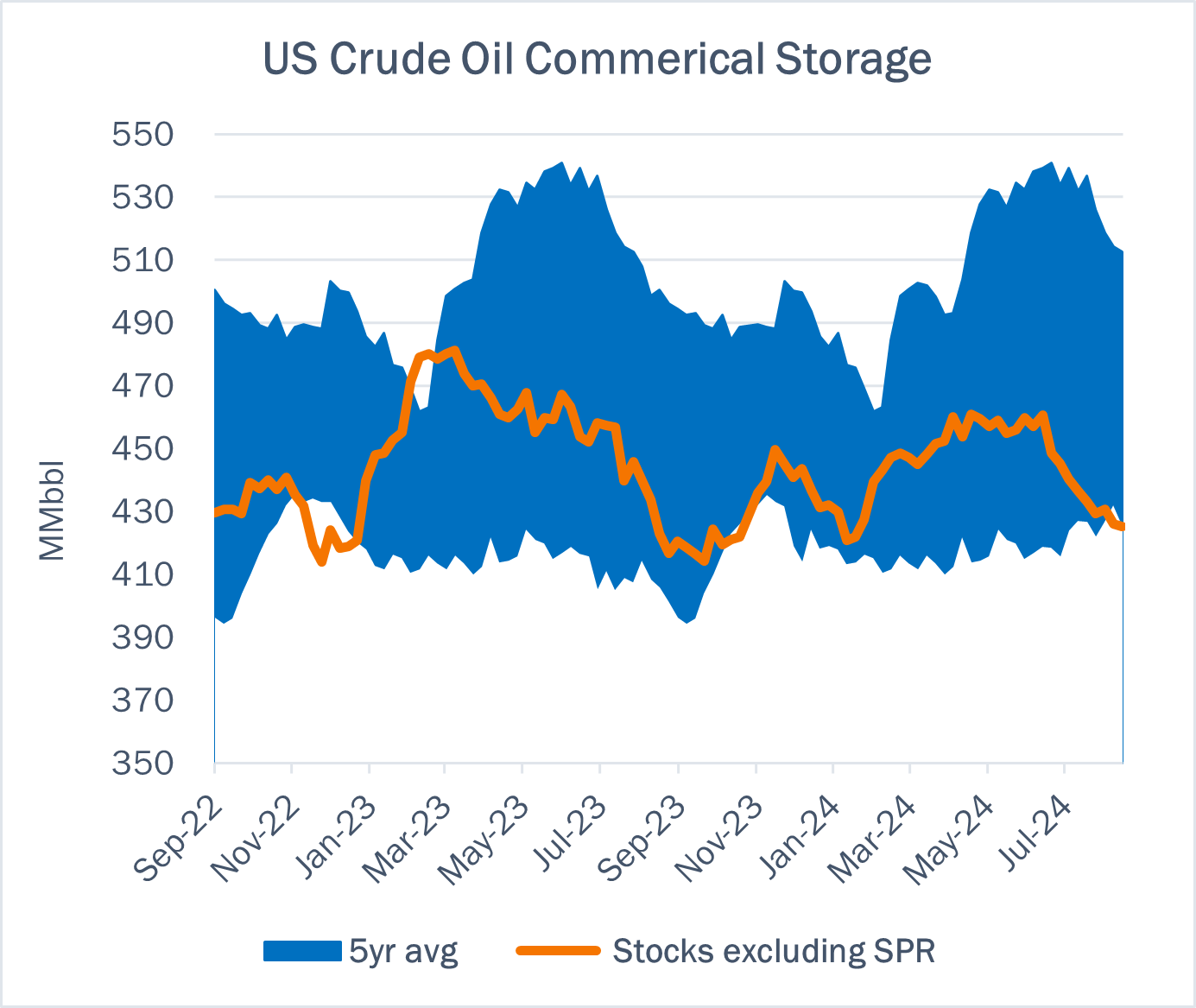

East Daley expects a 417 Mbbl withdrawal in commercial and Strategic Petroleum Reserve (SPR) inventories for the week ending September 13. We expect total US stocks, including the SPR, will close at 798 MMbbl.

The US natural gas pipeline sample, a proxy for change in oil production, decreased 1.6% W-o-W across all liquids-focused basins. Samples decreased by 48% (~1.1 Bcf/d) in the Gulf of Mexico, 6.4% in the Williston, and 1.7% in the Rockies. The increase was offset by samples increasing 1.45% in the Eagle Ford and 1.45% in the Permian. The Gulf of Mexico and Williston Basin have a high correlation between gas volumes and crude oil volumes, whereas the correlations for the Permian and Eagle Ford are less than 45%. We expect US crude production to remain flat at 13.3 MMb/d.

According to US bill of lading data, US crude imports decreased by 551 Mb/d W-o-W to 6.32 MMb/d. More than 60% of the supply originated from Canadian pipelines into the US, with the remainder largely coming from ships carrying crude from Mexico, Venezuela and Argentina.

As of September 6, there was ~226 Mb/d of refining capacity offline, including downtime for planned and unplanned maintenance. EDA expects gross crude inputs into refineries to decrease by ~174 Mb/d W-o-W, coming in at 16.6 MMb/d.

Vessel traffic monitored by EDA along the Gulf Coast increased W-o-W. There were 28 vessels loaded for the week ending September 13 and 22 the prior week. EDA expects US exports to be 3.77 MMb/d.

The SPR awarded contracts for 2.77 MMbbl to be delivered in September 2024. The SPR has 374 MMbbl in storage as of September 13, 2024.

Regulatory and Tariffs:

Presented by ARBO

Tariffs:

Hiland Crude, LLC. A new volume commitment shipper rate was established for shippers executing a TSA during the month of August for a term of at least 3 years with a minimum volume take-or-pay commitment. FERC No 5.41.0 IS24- 792 (filed Aug 30, 2024) Effective October 1, 2024.

Zydeco Pipeline Company The Zydeco and Marketlink Joint Tariff from Cushing, OK to Clovelly, Lafourche Parish, Louisiana and to St. James, Louisiana has been canceled. FERC No 16.6.0 IS24- 780 (filed July 31, 2024) Effective October 1, 2024.