Executive Summary:

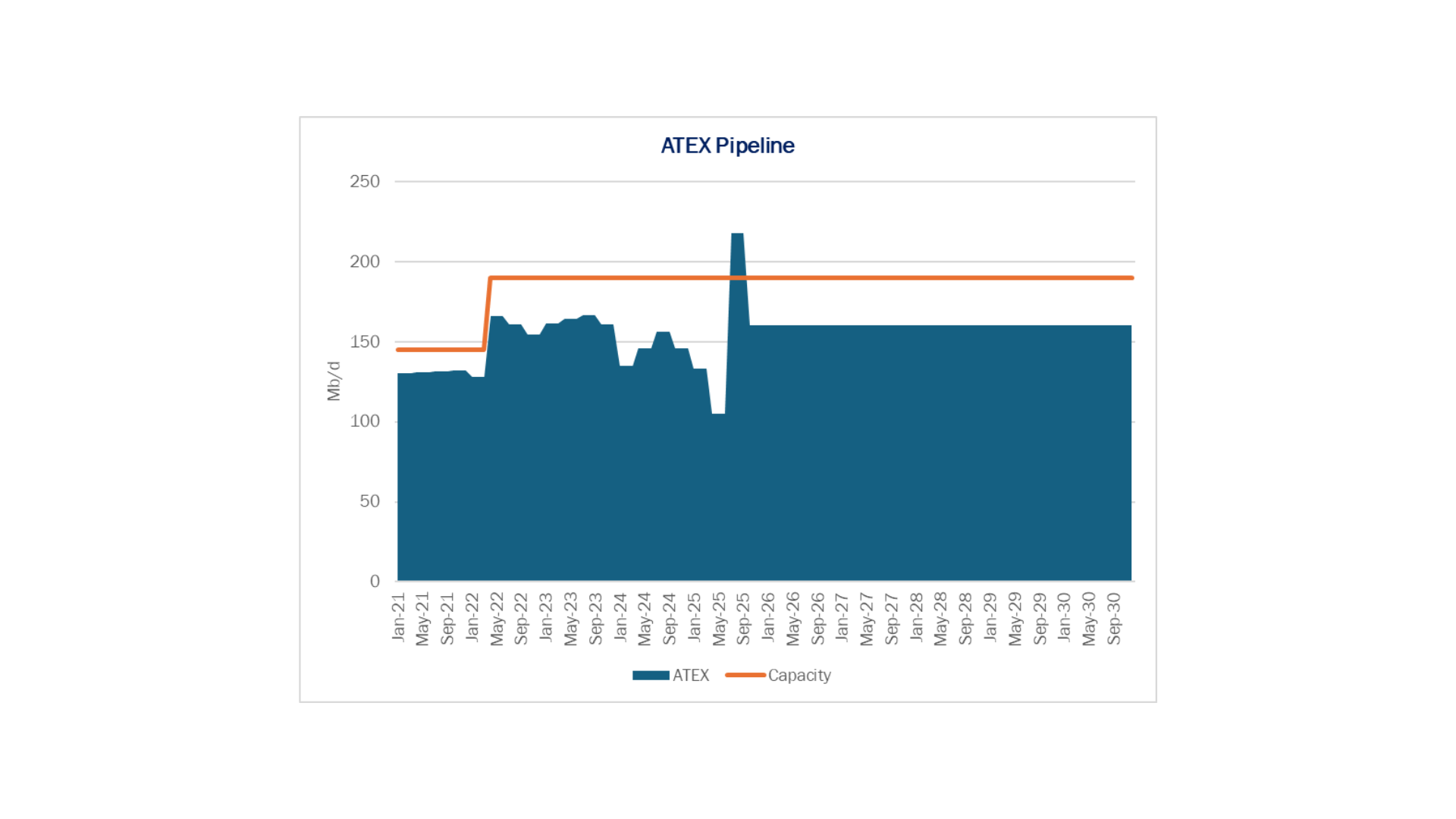

Infrastructure: ATEX Pipeline volumes doubled in 3Q25 to 218 Mb/d, gaining from the start of Enterprise’s Neches River Terminal.

Exports: LPG exports were steady through the week ending Dec. 5, while a significant decline at ET’s Nederland terminal resulted in a 64% W-o-W drop in total ethane exports.

Rigs: The total US rig count decreased during the week of Nov. 30 from 513 to 510. Liquids-driven basins lost 1 rig W-o-W, falling to 383.

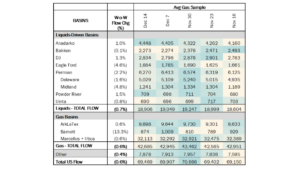

Flows: US natural gas volumes in pipeline samples averaged 69.5 Bcf/d for the week ending Dec. 14, down 0.6% W-o-W.

Calendar:

Infrastructure:

Ethane volumes shipped on ATEX Pipeline more than doubled in 3Q25, surging after the start of Enterprise Products’ (EPD) Neches River Terminal on the Texas Gulf Coast.

New filings at the Federal Energy Regulatory Commission (FERC) show ATEX (Appalachia-to-Texas) moved 218 Mb/d of ethane in 3Q25, up 107% from 105 Mb/d in 2Q25. Flows ran ~28 Mb/d above ATEX’s 190 Mb/d nameplate capacity, highlighting the system’s ability to flex in response to market conditions.

The gains underscore two structural advantages that are becoming increasingly important in today’s NGL market: ATEX’s operational flexibility, and Enterprise’s fully integrated Gulf Coast system.

We believe the startup of EPD’s Neches River Terminal was the primary catalyst for the jump. EPD in July started Phase 1 of the terminal near Beaumont, TX, creating a timely outlet for incremental barrels. ATEX feeds directly into EPD’s broader Gulf Coast distribution network, which ultimately supplies Neches River.

ATEX also likely gained from displaced ethane volumes in the Northeast. A furnace at Shell’s Monaca cracker in Pennsylvania exploded in June, cutting into regional demand. FERC filings show deliveries on Shell’s Falcon Pipeline, which feeds ethane to the Monaca facility, fell nearly 50% to 48 Mb/d in 2Q25. While Falcon throughput increased to 78 Mb/d in 3Q25, volumes remained about 20 Mb/d lower than the recent peak of 97 Mb/d in 4Q24.

EPD was well positioned to arbitrage the regional dislocation, pulling discounted Northeast ethane south to fill its new export capacity. Shell also has some reserved capacity on ATEX, and may have used the pipeline to offload stranded barrels during the Monaca outage. In effect, ATEX functioned as a pressure-release valve, linking Appalachian oversupply with new waterborne demand.

Why this matters: The jump in 3Q25 demonstrates that ATEX can operate above its stated nameplate when market incentives are strong, and that EPD’s integrated footprint allows it to rapidly redirect barrels across regions.

East Daley does not view 3Q25 flows as a new steady state, and we expect volumes on ATEX to retreat toward historical levels when Monaca returns to full operations. However, the setup is instructive. As US ethane markets grow more entwined with exports, similar displacement episodes are likely to occur during cracker outages, maintenance events, or step-changes in export demand.

The Permian Basin at a Crossroads: Download Why This Pipeline Boom is Different

The Permian’s next big buildout is already taking shape — but this time, the drivers aren’t producers chasing oil. East Daley’s latest white paper reveals how gas demand from AI data centers, LNG exports, and utilities is rewriting the midstream playbook. Over 9 Bcf/d of new capacity and $12 billion in investments are reshaping flows, turning the Permian into a gas powerhouse even as rigs decline. Read Part II: Why This Pipeline Boom is Different

In other words, this is not the new normal, but it may be a preview. ATEX’s role is evolving from a steady baseload pipe into a swing asset that clears regional imbalances, reinforcing the strategic value of integrated systems as US NGL markets become more globally connected.

Exports:

LPG exports were steady for the week ending Dec. 5. Ethane exports, however, saw a significant pullback across terminals, with ET notably exporting zero ethane at the Nederland terminal. This drove a significant 64% W-o-W decline in total ethane exports, contributing to a 12% decrease in total US NGL exports.

Rigs:

The total US rig count decreased during the week of Nov. 30 from 513 to 510. Liquids-driven basins lost 1 rig W-o-W, falling from 384 to 383.

- Anadarko (+1): Landmark Resources

- Uinta (-1): Fourpoint Resources

- Permian:

-

- Delaware (+1): EOG Resources

-

- Midland (-2): Exxon, Diamondback Energy

Flows:

US natural gas volumes in pipeline samples averaged 69.5 Bcf/d for the week ending Dec. 14, down 0.6% W-o-W.

Major gas basins declined 0.6% W-o-W to average 42.7 Bcf/d. The Haynesville sample gained 0.6% to 9.7 Bcf/d, while the Marcellus+Utica slid 0.6% to 32.1 Bcf/d. The Barnett sample declined 13.3% W-o-W.

Samples in liquids-focused basins decreased 0.7% to 18.9 Bcf/d. The Permian sample declined 2.2% to 6.3 Bcf/d, and the Eagle Ford sample fell 4.6% W-o-W.

Calendar: