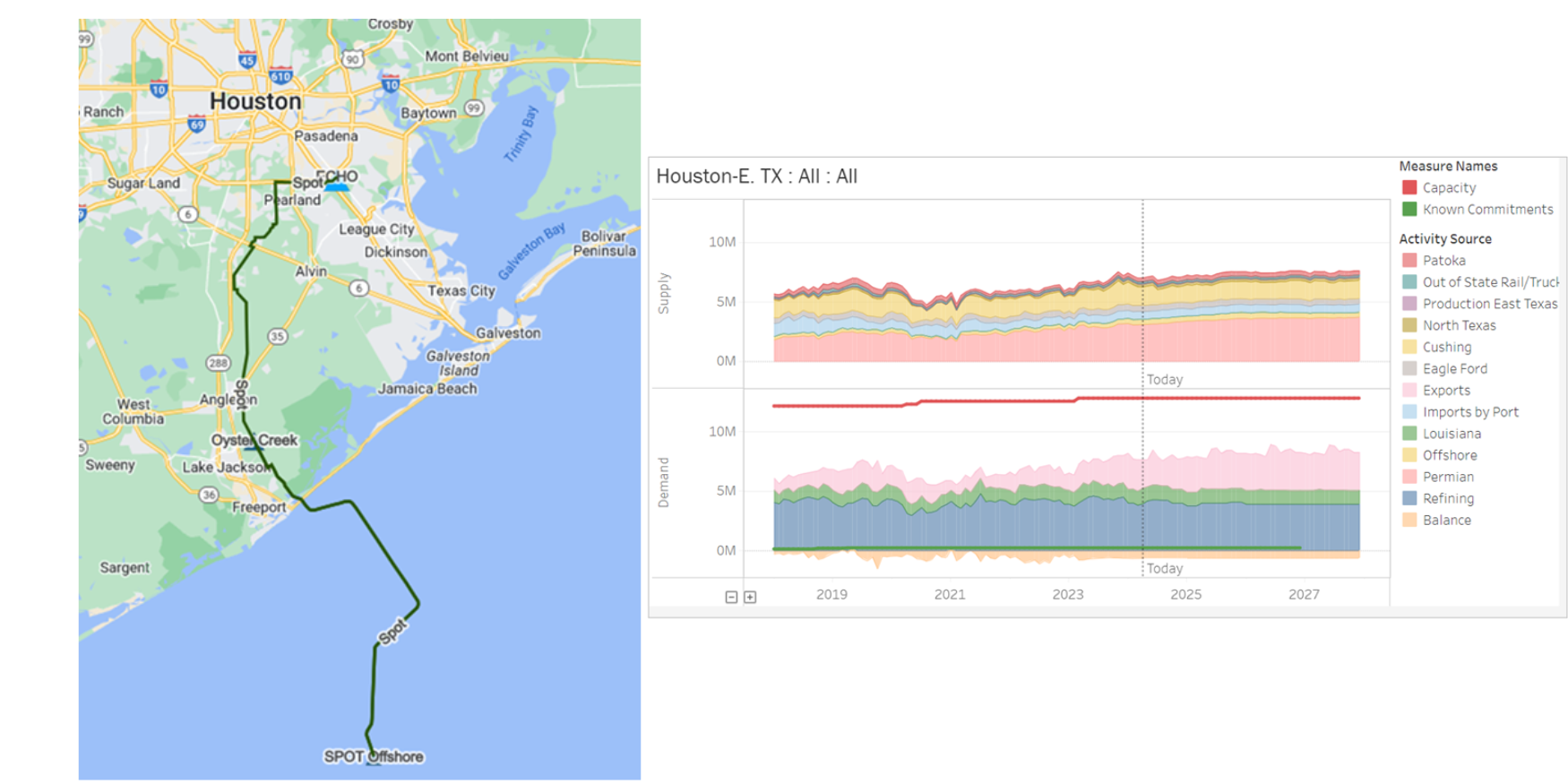

Enterprise Products (EPD) has secured a deepwater port license for its Sea Port Oil Terminal (SPOT) after a favorable appellate court ruling, moving ...

Read

Energy Insights and News

18 Apr

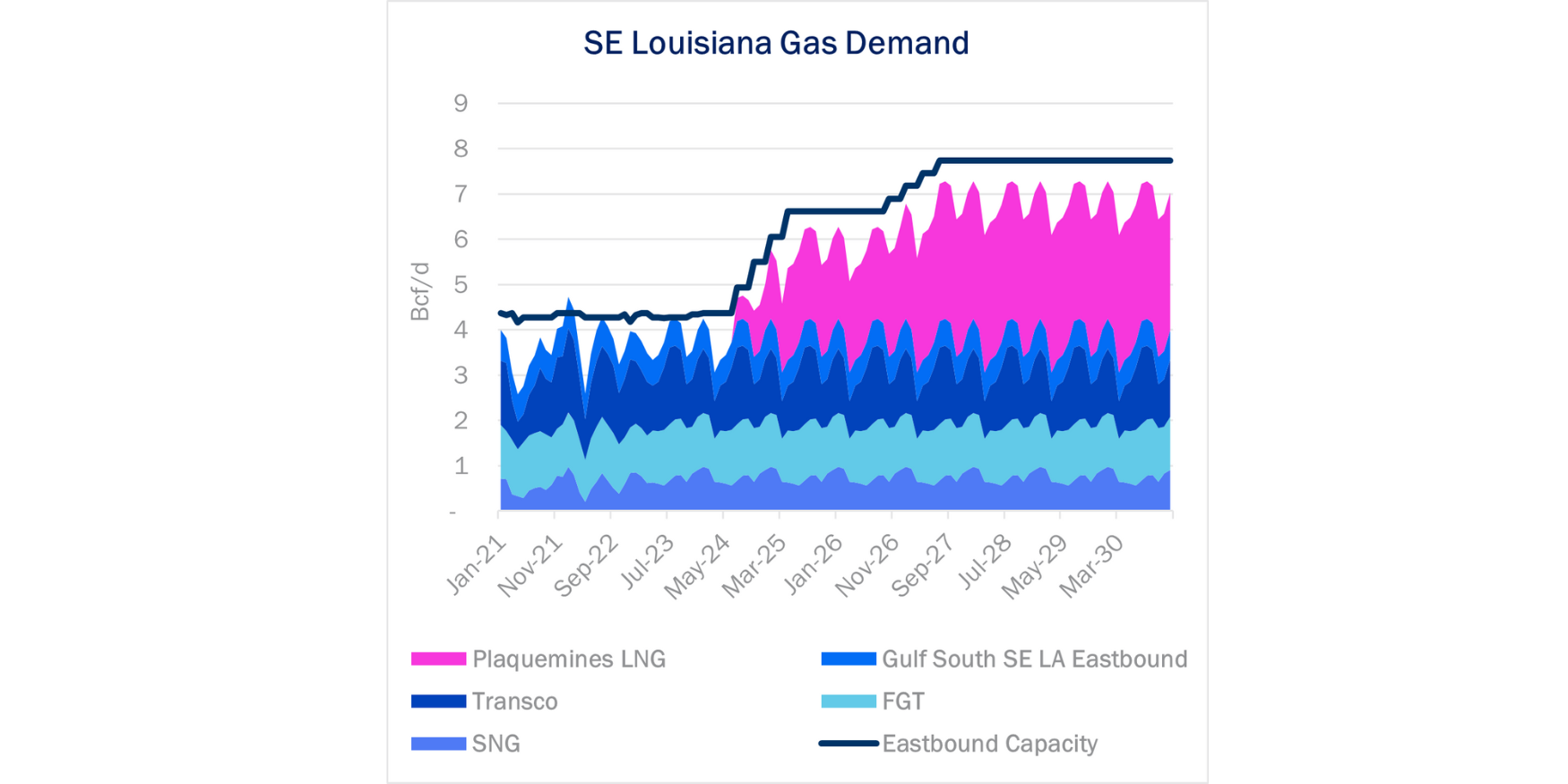

Federal regulators have given Enbridge (ENB) the green light to start a new pipeline serving an LNG project finishing construction on the Louisiana ...

Read

11 Apr

Unshackled at last, producers in Western Canada plan to raise crude oil output in anticipation of the new Trans Mountain Pipeline expansion (TMX). In ...

Read

9 Apr

Chesapeake Energy (CHK) and Southwestern Energy (SWN) have postponed the closing date of their E&P ‘super-merger’ following a request from the ...

Read

5 Apr

The Permian Basin will drive new NGL supply growth in 2024, as East Daley Analytics highlighted in our recent 1Q24 NGL webinar. Yet it may come as a ...

Read

4 Apr

Crude oil pipeline takeaway out of the Williston Basin is much tighter than it appears at first glance. As Bakken oil production continues to grow, ...

Read

Subscribe to

the Daley Note

SUBSCRIBE

Posts by Topic

Recent Posts

Enterprise Secures SPOT Permit After Court Ruling

April 19, 2024